Sovereign ESG resilience key for bond investors turning back to emerging markets

by Emma Whiteacre and Eileen Gavin,

This insight draws on analysis from our Sovereign ESG Ratings 2023-Q1 update research report. Download the report now if you would like to read the full analysis.

Rising debt and political uncertainty among warning signs for emerging market investors in latest Sovereign ESG Ratings

With emerging market bond issuance stepping up in January, thanks to easing inflation and interest rate expectations, as well as accelerating growth, risk aversion is receding and appetite is back. But high levels of indebtedness, elevated political and geopolitical uncertainty, and mounting climate-related risks warrant vigilance. ESG factors that influence a country’s resilience to such challenges will be key differentiators in portfolio performance.

The latest data from our award-winning Sovereign ESG Ratings, which cover 198 countries, shines a light on some of the key issues influencing investment profiles. Eleven countries, including Nigeria, Côte d’Ivoire and Venezuela, had their headline ratings upgraded, while 20 including Brazil and Sri Lanka were downgraded. For countries with unchanged ratings, the scores of 42 improved, while 81 declined.

Amid debt distress and other challenges, some African sovereigns advance on ESG

In sub-Saharan Africa, the average Sovereign ESG score is 35/100 (with a score of 100 representing best performance) versus a global average of 51/100. Debt distress remains an urgent concern, with Ghana, Ethiopia, Chad and Zambia already in debt restructuring talks and others still vulnerable. This is a difficult backdrop for ESG progress and 17 countries across the region have seen their scores worsen. But encouragingly, ten countries’ scores increased, and three major markets have had their headline rating upgraded.

Côte d’Ivoire’s overall rating moved from 2 to 2+, where 5+ is considered the strongest possible, thanks to both Social and Governance factors.

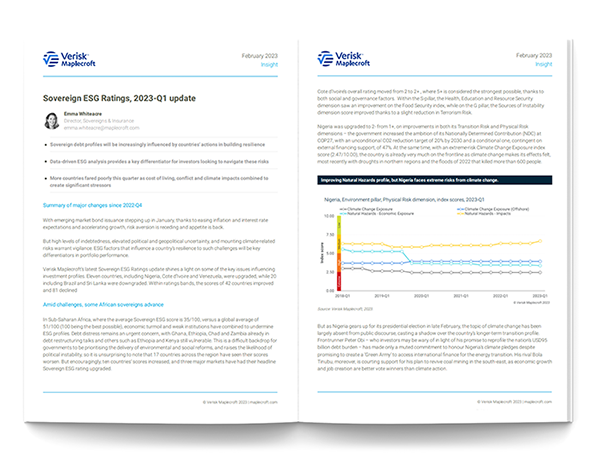

Nigeria was upgraded to 2- from 1+, on improvements in its Transition Risk and Physical Risk Dimensions under the E pillar. But though the country is very much on the front line, the topic of climate change was largely absent from public discourse ahead of the general election in late February, casting a shadow over the longer-term transition profile.

Uganda, likewise, was upgraded to 2- (from 1+), driven in part by a better (albeit still extremely low) deforestation score.

Looking north, good news stories were hard to come by across the Middle East and North Africa, with downgrades for the Occupied Palestinian Territories, Libya and Iran. The devastating earthquake in Turkey and Syria occurred after our Ratings’ underlying risk indices updated, but its effects were foreshadowed by a fall in Turkey’s Natural Hazards – Impacts Index and a recent decline in the Corruption Index. We anticipate a broad-based deterioration in the country’s metrics in our next update, suggesting peril for President Erdogan’s re-election bid in May.

Notable ESG improvers in developed Europe but Russia-Ukraine conflict still making its mark

Across Europe, the Russia-Ukraine war continues to drive negative trends and particularly to weigh on Central and Eastern European countries most exposed to cost of living and societal impacts. Twenty-three countries across the region saw falling scores this quarter. Of the nine that saw scores improve, only Belarus (ESG rated 3) and Romania (4) were below high-income status.

Romania’s score climbed one point thanks to anti-corruption measures supporting judicial independence. Belarus’s repressive crackdown on activism reduces the risk of destabilising civil unrest, supporting the Sources of Instability score. Its Democratic Governance performance on the other hand is dismal.

Three developed markets saw one-notch rating upgrades – Ireland (to 5), driven by improvements across its E pillar; Italy (to 4+) on G; and Spain (to 5-) on improvements across all pillars.

Slovenia (5+), the highest-ranked sovereign across all markets, and Greece (4) both weakened on lower Governance scores. Bosnia and Herzegovina (4+), the second-best ESG performer in the Balkans, is suffering with water pollution challenges that prompted a decline on the E-pillar.

Russia’s (2) ESG profile continues to weaken (down 1 point to 28/100) a year into its war against Ukraine on factors relating to the conflict, with marginal declines across all Environment Dimensions and on Labour Rights.

Ukraine (3) has also seen its score fall because of a worsening Social pillar, amid a deteriorating human rights profile. While clearly the victim in a brutal and unjust war where human rights abuses are manifold, the state’s own mediocre track record has been exacerbated and amplified by the conflict.

Rising civil unrest poses problems for Asian sovereigns

Across Asia, nine countries have seen an improvement in their ESG scores, while 11 have witnessed a deterioration. A dominant theme is rising civil unrest, with eight countries seeing lower scores for Sources of Instability, led by China (2+) with a 9-point fall due to protests over its Zero Covid policy that may presage more activism in the future. But Tajikistan’s (3-) score recovered this quarter after protests last year, as the state’s determination to suppress civil unrest at all costs limits scope for regime change.

Elsewhere, disparate drivers of unrest include the chaos around debt distress in Sri Lanka (downgraded to 2 from 2+), and rising food and fuel prices in Bangladesh (2-) and Indonesia (2+).

Turkmenistan has been downgraded from 2+ to 2 on a poorer Environment score on Water Pollution, reflecting how aridification, salinisation and agricultural pollution are presenting major challenges in Central Asia as temperatures rise by far more than the global average.

Politics driving ESG outcomes in Latin America

In Latin America nine countries have seen marginal improvements and 12 have weakened. One upgrade – Venezuela – and one downgrade – Brazil – dominate the story, as the capital market outcast and the one-time poster child manage acute challenges.

Venezuela, the weakest ESG performer across the Americas with a score of 22/100, has been upgraded from 2- to 2 on improving Food Security, a product of a nascent economic recovery.

Brazil has been downgraded to 3- due to both Environmental and Governance declines. The administration of Luiz Inacio Lula da Silva is expected to take a far more pro-active stance to address climate change and deforestation than his predecessor, which will underpin demand for its first sovereign green bond issuance this year.

However, executing policy and governing a bitterly divided nation will not be straightforward, and investors will remain cautious on fiscal and social uncertainty.

Spotting underlying ESG signals crucial for active sovereign investors

With the aftershocks of the Covid-19 pandemic and Russia’s invasion of Ukraine continuing to be felt, sovereigns everywhere are feeling the strain – and especially so in emerging markets. As a result, some are putting ESG issues on the backburner. But others continue to make progress, with many looking to ‘green’ their budgets and public debt issuances, in support of environmental and social progress. For sovereign debt investors, identifying issuers with these traits, and the underlying signals that suggest their direction of travel, will be a key factor in effectively navigating the market’s movements. This is where our Sovereign ESG Ratings can make the difference.

About our Sovereign ESG Ratings

Our award-winning Sovereign ESG Ratings offer investors a standard-setting method for measuring and tracking environmental, social and governance (ESG) risks for government debt issuers. Built on a foundation of 35 of Verisk Maplecroft’s proprietary risk indices, the Ratings employ a novel quantitative scoring methodology, based on cluster analysis, that accurately identifies material changes in an issuer’s sustainability profile.

The Ratings assess 198 countries across nine dimensions of ESG risk, with a quarterly time series beginning in 2017. For each quarter and dimension the clustering algorithm assigns each country a probability that it belongs in Weak, Moderate or Strong clusters, based on that country’s performance on the underlying indices within that dimension. The clustering results are used to calculate an overall 0-100 ESG score per country, in addition to E, S and G pillar scores. Those scores are then converted to ESG and pillar Ratings on a 15-notch scale, ranging from 1- to 5+ (worst to best performing).

In recognition of our Sovereign ESG Ratings, we were named Best Specialist ESG Ratings Provider at the ESG Investing Awards 2023.