Geospatial ESG investing

Learn more

The G in Sovereign ESG

The governance pillar continued to drive changes in our Sovereign ESG Ratings in the third quarter, reflecting the intense pressures of 2022. Sri Lanka’s political crisis saw the country deteriorate the most in our dataset in Q3.

But beyond Sri Lanka, efforts to avert an EM sovereign debt crisis more broadly may also be hampered by weak governance.

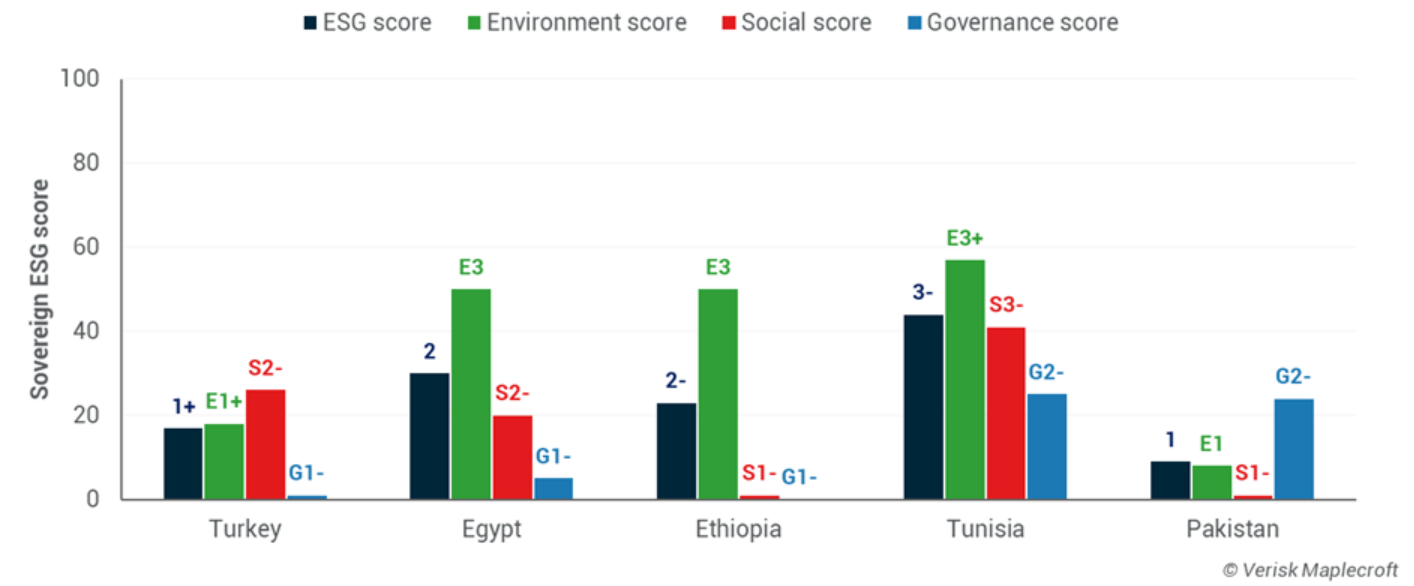

Debt distress is spreading through the EM universe, from vulnerable Asian and Sub-Saharan African countries such as Pakistan and Ethiopia to mid-ranking MENA sovereigns such as Egypt and Tunisia. Tellingly, the IMF is in emergency talks with many of these. But the dire governance profiles of these countries, including their long-term institutional weaknesses, have the potential to undermine the effectiveness of any IMF lending programme. The same governance shortfalls, critically, will also weigh on bondholder confidence.

Moreover, governance is looking uneven beyond those in immediate fiscal distress. G pillar scores declined in several of the Central Asian and Eastern European countries that are feeling the impacts of the Russia-Ukraine war. These include the likes of Armenia, Azerbaijan, Bosnia and Herzegovina, Bulgaria, Georgia, Hungary and Serbia.

In Africa, meanwhile, Kenya’s slight decline on the G pillar reflected the August election, while Tanzania also saw a deterioration in its score, which we are keeping an eye on.

Across the Atlantic, looking beyond Argentina’s latest economic and political crisis, governance in other Latin American sovereigns is also under pressure as the region’s political pendulum swings once more. Countries affected include Chile, Colombia, Peru and Brazil, the latter gearing up for important presidential elections in October.

Finally, in Asia, third quarter governance scores also registered some deterioration in the likes of India, Indonesia and notably also China, where protests have been bubbling up against pandemic restrictions and, more recently, the property crisis.

With global food and energy insecurity spreading, and recession/stagflation already evident in the US and Western Europe (with inevitable negative impacts for EMs), we expect pressure on Sovereign ESG scores to persist to year-end and into 2023, with even DM governments struggling to keep a lid on social demands.

Chart of the week

Quote of the week

We don’t need to cut down even one more tree to plant soybeans. We don’t need to cut down one more tree to plant corn. We don’t need to cut down a single tree to plant sugarcane or raise cattle.

Lula da Silva

Brazil’s twice former president Lula da Silva (2003-2010) pledges to stop deforestation if returned to office for a third time in October’s general election, 22 August 2022

What we’re reading

- Democracy in Brazil, Chatham House, 17 August 2022

- Liz Cheney already has a 2024 strategy, The Atlantic, 17 August 2022

- Setting standards will help Asian social bond market to flourish, Nikkei Asia, 17 August 2022

- Public sector must play major role in catalyzing private climate finance, IMFBlog, 18 August 2022

- Saudi ambition helps Islamic bond market evade the global gloom, Bloomberg Markets, 18 August 2022

- William Ruto is declared Kenya’s next president, The Economist, 18 August 2022

- Abrdn: EU Taxonomy social proposals could have 'drastic' impact, Environmental Finance, 19 August 2022

- Finance groups risk being kicked out of Mark Carney-led climate coalition, FT, 22 August 2022

- EU Regulator throws weight behind prospective ESG benchmark, Responsible Investor, 22 August 2022