Civil unrest risks overshadow bumper election period

Inflection Points

by Jess Middleton,

We started the year by analysing data from our suite of country risk indices to highlight the key trends and signals shaping the global risk environment. We found that risks had increased at a global level across 67 of the 123 political, human rights and economic issues tracked by our data in 2023, compared to 49 that saw an improvement.

As we head into the second quarter of 2024, it’s clear the world remains in a state of upheaval. Surging geopolitical tensions, economic volatility and heightened political unrest amid a slew of elections are just a few of the interconnected risks that businesses are grappling with. The recent escalation of hostilities between Israel and Iran, which occurred after our latest data update, threatens to inject new turbulence into an already fragile risk landscape.

In this article, we’ve used our latest data to pinpoint a few key areas where these dynamics have translated into major shifts within our Global Risk Data.

Unrest likely as world prepares for slew of significant votes

In January, we predicted that longstanding socioeconomic tensions could come to the boil in 2024 as countries home to more than 4bn people prepare to head to the polls.

This trend hasn’t quite played out within the data so far. Some 28 countries registered a significant decrease in risk on the latest edition of our predictive Civil Unrest Index (CUI), in part due to easing inflation, compared to 13 that registered a significant increase.

That said, issues such as political polarisation and rising inequality persist in much of the world, and the global economic outlook remains volatile - particularly given the recent surge in Israel-Iran tensions and the related risk of a wider regional war in the Middle East. As such, civil unrest risks remain high as the world gears up for a host of significant elections.

Indeed, 32 of the 44 countries set to hold elections between now and the end of the year are rated high or very high risk on the CUI, which forecasts the likelihood of large-scale protests over the next 12-months. These include the US, which ranks 1st and highest risk globally, as well as India (4th) and Mexico (5th), both of which have votes scheduled later this quarter.

The EU, meanwhile, accounts for four of the 10 highest risk countries globally, including Germany (2nd), France (3rd), Spain (8th) and Italy (9th). June’s EU Parliament election could serve as a flashpoint for farmers’ protests, which have surged throughout the bloc this year amid tensions over tightening climate rules and cheap food imports.

Resource nationalism surges in mineral-rich countries

One of our predictions that did play out last quarter relates to rising resource nationalism in Africa. At the start of the year, we warned that the continent’s resource-rich countries could push for greater control over their natural resources as the global rush for critical materials accelerates.

Five sub-Saharan African countries have registered a significant increase in risk on our Resource Nationalism Index (RNI) since then. This includes Tanzania, where the government’s plans to ban unrefined lithium exports have seen the country drop to 16th highest risk globally in the dataset.

Elsewhere on the continent, Niger plummeted 46 positions to 96th highest risk. The shift resulted from the military government’s decision to suspend granting new mining licenses in the country, which serves as a major provider of the uranium ore needed to fuel nuclear reactors.

But rising resource nationalism isn’t restricted to Africa. Both Kazakhstan and Chile, major producers of critical minerals like copper, lithium and zinc, saw a significant increase in risk on the latest edition of the RNI. Kazakhstan now ranks as the 4th highest risk country globally, down from 31st at this stage last year. Chile, meanwhile, fell 13 positions to 42nd highest risk, down from 95th as recently as 2022-Q2.

Figure 2: Resource nationalism risks present in all regions

“The ongoing push from states to increase the benefits they derive from their natural resources throws up a host of challenges for global businesses,” says our Head of EMEA Hugo Brennan. “From miners having to shoulder higher costs associated with domestic beneficiation requirements through to end-users assessing how these dynamics might impact their supply chain risk exposure.”

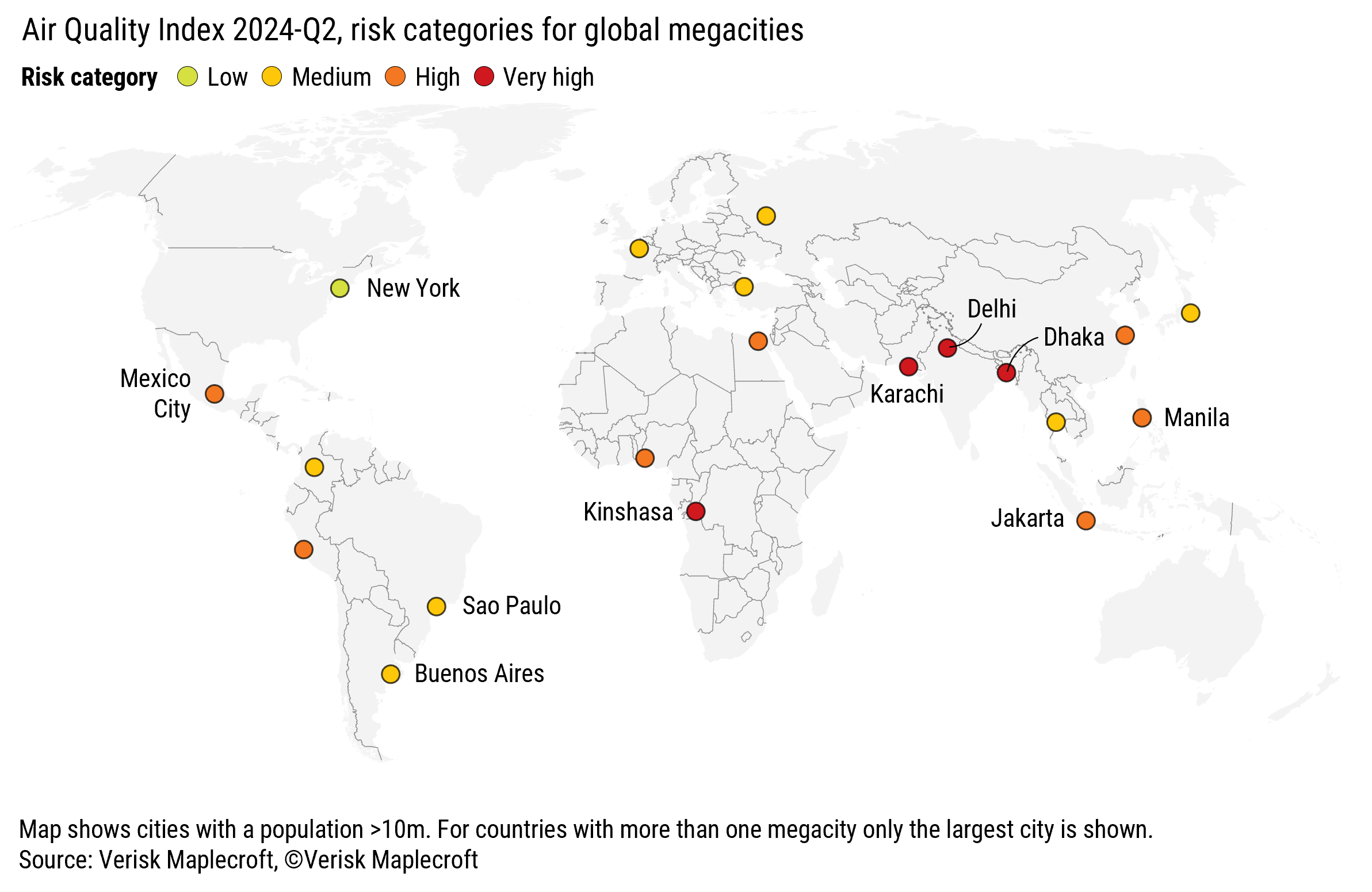

Half of world’s major cities exposed to high levels of air pollution

Pivoting onto our Environmental Risk Dataset, new data from our Air Quality Index suggests that some progress is being made at a global level when it comes to reducing levels of air pollution.

When looking at the 578 global cities with a population over a million, 71 saw a significant decrease in risk on the latest edition of the index, compared to just nine that saw a significant increase.

But drilling down further shows there is work to be done in terms of improving air quality in the world’s major urban hubs. Some 276 cities, home to just under a billion people, fall within the two highest risk categories of the index. Zooming into the world’s megacities (cities with a population over 10m) reveals that major metropoles like Delhi, Dhaka and Kinshasa are among those facing the highest risk.

The immediate concern associated with poor air quality is the threat to human health. Studies have linked air pollution to a range of adverse health problems, such as respiratory illnesses and cancers stemming from carcinogens. But it also poses challenges for businesses operating in high risk areas.

“Clearly, there are financial, legal and reputational penalties facing organisations associated with air pollution,” says our Head of Climate and Resilience Will Nichols. “But companies must also consider the associated health and productivity impacts for their workforce and supply chain.”

Data key to navigating volatile risk environment

As ever, the list of issues highlighted above represents a small subset of the complex challenges facing businesses. In the months ahead, companies will need to monitor not only these threats, but a host of other systemic risks – including the wider ramifications of the escalating conflict in the Middle East. Those that embed cutting-edge data and analytics will stand the best chance of bolstering the resilience of their operations and supply chains in an increasingly volatile risk environment.