Africa’s debt dependent resource producers falling into China’s orbit

by Aleix Montana,

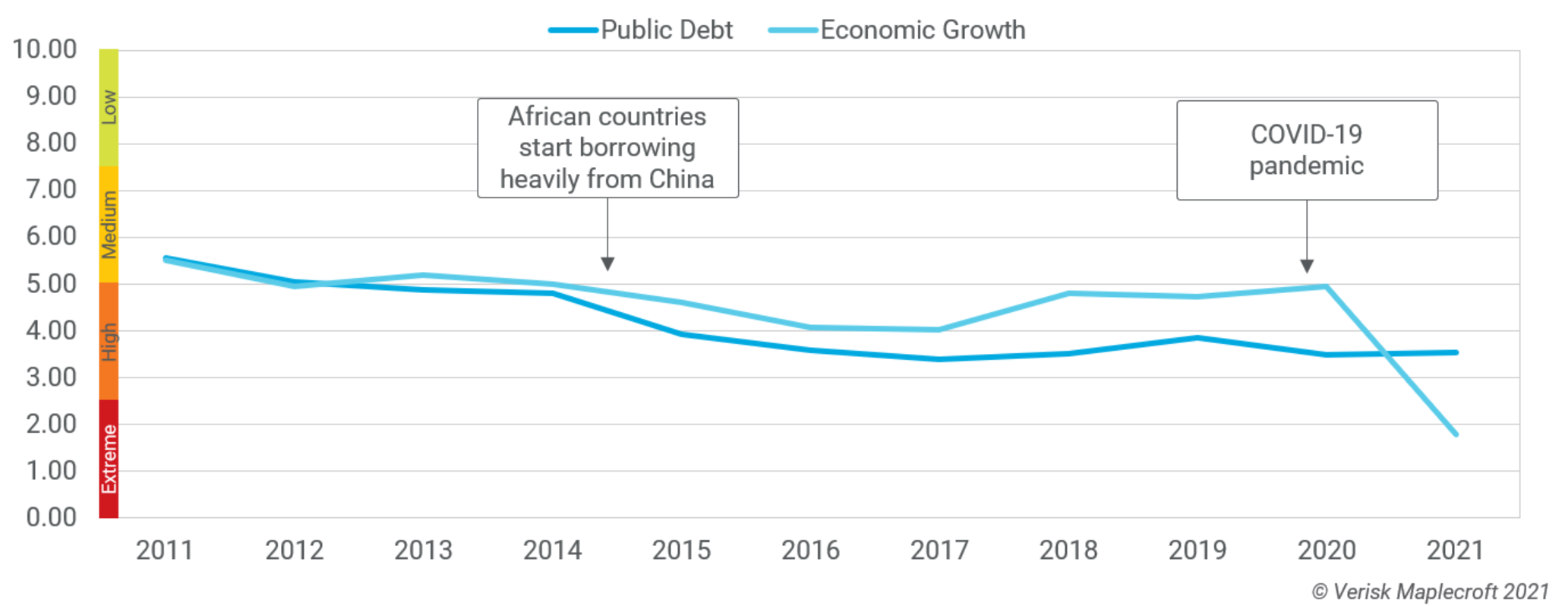

Public debt in sub-Saharan Africa has increased dramatically in the last ten years, with countries borrowing heavily from China to fund major infrastructure projects. However, the decrease in commodity prices and the slowdown in the African economy since 2015 has hindered their capacity to repay public debt. Debt distress risk in the region has further increased due to the economic impact of the COVID-19 pandemic, which triggered Zambia’s default in 2020-Q4.

In addition, debt conditions from Chinese creditors are often opaque and established on a case-by-case basis. Thus, investors and stakeholders fear that China could take advantage of the current debt crisis to acquire the control of strategic assets, locking out Western companies, and leaving African countries in a state of dependency.

China’s role in the African debt crisis

Zambia’s default shows that, apart from the total amount of debt, the structure and composition of creditors also play a significant role when determining debt risk. The popularity of Chinese creditors has created a more diverse creditor base than the historical primarily Paris Club bilateral lenders, which complicates the resolution of repayment conflicts.

Since Chinese creditors are often not transparent, Western bondholders are more likely to reject potential debt relief packages in countries borrowing from China, fearing that the debt relief will be used to repay Chinese loans. Therefore,

countries that have received considerable loans from China are likely to experience tensions between Western bondholders and Chinese creditors.

Moreover, investors and stakeholders in Africa tend to be preoccupied by the so-called “debt-trap diplomacy”. This refers to the idea that China has the long-term goal of obtaining access to key assets and commodities by tying African countries to debt contracts that they will not be able to repay. However, there is little evidence that China is pardoning African countries from their debt obligations in exchange for control of strategic assets. So far, the most common renegotiation strategy by Chinese creditors is the deferrals of payment deadlines.

Yet, access to natural resources plays a central role in the repayment conditions of some Chinese loans. China often offers resource-backed loans to resource-rich countries, using commodities as a repayment method or as a collateral. This type of loans is often predicated on the future production of a natural resources such as cocoa, tobacco, oil or copper.

Resource-backed loans are often attractive for African countries with limited access to capital markets, since they can be used to finance infrastructure projects and are perceived as a cheaper financing method. However, these loans can also increase fiscal pressures in highly indebted countries and disrupt their commodity production. Repayment deals based on the future value rather than on the quantity of a commodity are especially risky for the borrower, since a decrease in commodity prices in the global market would require an artificial increase in its production to cover the debt obligations.

Find out more about our Country Risk Intelligence

Not all countries with high debt risk are equally exposed to reserve-based lending from China

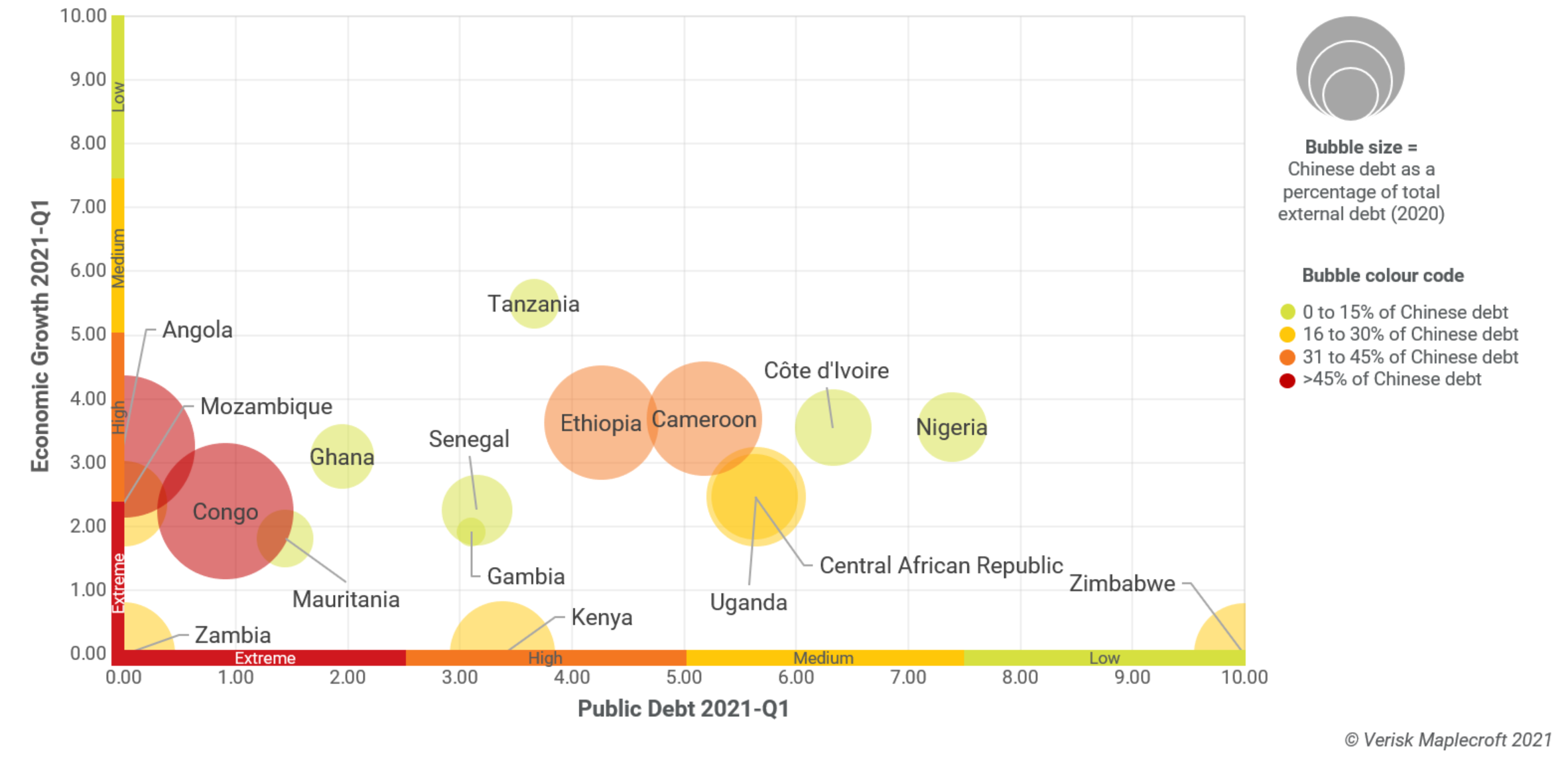

Debt levels in oil-exporting countries such as Congo and Angola are particularly concerning, since the collapse in global oil prices has led to the devaluation of their national currencies. This makes debt repayments denominated in foreign currency relatively more expensive. In addition, the use of reserve-based lending adds an extra layer in the complicated debt landscape of commodity-dependent countries, further increasing the risk of debt distress.

In the chart below, we show that Congo and Angola are the most exposed to the consequences of reserve-based lending. Apart from being two of the countries with the highest risk in public debt and economic growth in our indices, they are two of the countries that have borrowed more heavily from China. China’s presence has also played an important role in the debt sustainability of Zambia and Mozambique, where China holds 26 and 18 % of external public debt respectively.

In contrast, other highly indebted countries such as Mauritania and Ghana are less exposed to the risks of resource-backed loans, since Chinese debt only represents less than 15 % of the total external debt. It is also worth mentioning that, while risk to default is lower in Ethiopia, Cameroon, Kenya and Uganda, they have borrowed heavily from China and could also be exposed to some of the risks of resource-backed loans.

However, not all Chinese loans follow a resource-backed approach and its application varies country by country. While only some specific projects in Nigeria and Ghana follow the reserve-based lending strategy, the model is more common in countries such as Angola and Congo.

Looking ahead

As countries in sub-Saharan Africa continue to suffer from the economic impact of the pandemic, we expect the risk of debt distress to increase, especially in countries with large amounts of Chinese loans. The recent increase in oil prices will provide some form of temporary relief and ease the situation for oil-dependent countries.

However, Angola and Congo are especially vulnerable, since they present high debt levels, a severe economic recession and have borrowed significant amounts from China using resource-backed loans. The case of Angola is particularly concerning, since it is estimated that around 75% of the total Chinese debt is funded this way, often secured by oil exports. Angola is the country with the highest amount of Chinese loans, spread across 100 projects to finance oil and power state-owned enterprises.

Companies and investors in Angola can expect credit ratings to further deteriorate. As Angola is being pushed into debt restructuring in 2021, commercial creditors are hoping that a post-pandemic oil price recovery will enable the country to meet its obligations. However, the oil industry will take time to recover and public debt in Angola is in a very critical situation.