Brazil, India, Saudi Arabia among largest emitters with most to lose from climate change

The Trendline

by James Lockhart Smith and Will Nichols,

Unless the current emissions trajectory changes, 13 of the 30 countries responsible for almost 90% of carbon pollution could be facing some of the severest impacts of climate change, especially from heat.

Data from our Climate Hazard Index, which forms part of our Climate Risk Dataset, shows that major emitting markets, such as Brazil, India, Indonesia, Malaysia, Saudi Arabia, Thailand, Vietnam and the UAE, will be among the most exposed countries globally for climate impacts if emissions policies stay as they are. While not immune, the world’s two largest emitters, the US and China, should for the most part escape the very worst outcomes.

Climate Risk Dataset

Our Climate Risk Dataset provides organisations with a complete view of their global climate risk exposures. The dataset features our Climate Scenarios, which assess how climate hazards, such as heat, precipitation and sea level rise, will evolve over time across different emissions pathways. It also includes global risk indices covering climate-related socio-economic vulnerabilities and an array of transition risk issues, delivering a full-spectrum approach to your climate data needs.

Learn moreThe UNFCCC COP process might give the impression that countries are either drivers or sufferers of climate change. But our analysis reveals a clear overlap between those perpetuating global warming and the societies and economies set to face the harshest consequences.

One third of major emitters highly exposed to climate impacts

For more than a third of the world’s 30 largest emitters the future holds significant physical climate risks later in the century, even if global emissions-cutting efforts continue. While most major emitters driving global heating will suffer to some degree, our data identifies the carbon-heavy markets that will need to undertake extreme adaptation to protect their populations, societies and economies – particularly if, as predicted, mean surface temperatures breach the globally-recognised 2C threshold.

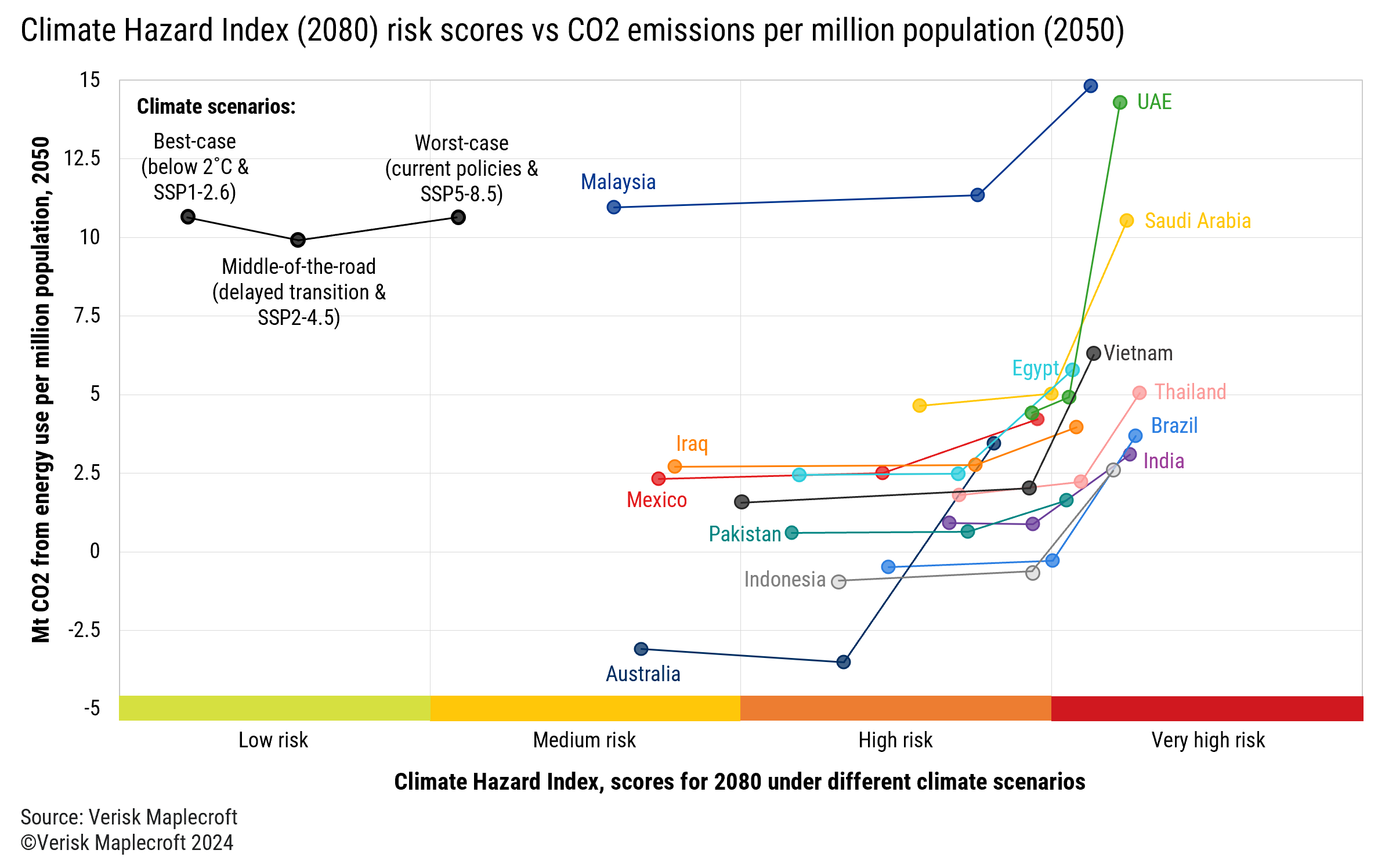

As shown in Figure 1, 13 major emitters will face ‘high’ or ‘very high’ levels of risk by 2080 across two or three of the emissions scenarios assessed by our Climate Hazard Index, which measures exposure to 16 chronic and acute climate risks, such as extreme temperatures, drought and severe storms, across seven time-horizons. Concerningly for most of these countries, the risks are significant even under the best-case climate scenario.

In terms of physical risk, four countries – Malaysia, Iraq, Mexico and Australia – stay above the critical ‘high’ risk threshold in the most optimistic scenario. But all four suffer much poorer outcomes under either middle-of-the-road or worst-case scenarios.

By pairing three physical risk scenarios with three transition risk scenarios for 2050 developed by the Network for Greening the Financial System (NGFS), a network of central banks and supervisors, the data also shows how policy decisions in the coming years will lock in physical risks later in the century. This matters most for Egypt, India, Indonesia, Pakistan, Saudi Arabia, Thailand, Vietnam and Brazil, which will likely experience some of the most significant impacts of climate change under all three scenarios, including the most optimistic pathway.

This should provide a clear incentive for these countries to cut emissions as soon as possible. A swift and managed energy transition could provide significant physical risk gains compared to a delayed or disorderly transition – where emissions-cutting policy measures could be imposed with little warning.

But some fossil fuel producers, especially in the Middle East, where the benefits of a low-carbon transition are less clear cut, may reason that the effort needed to achieve a low carbon future isn’t worth their while; a viewpoint that could undermine future international climate negotiations.

Rising heat an existential threat

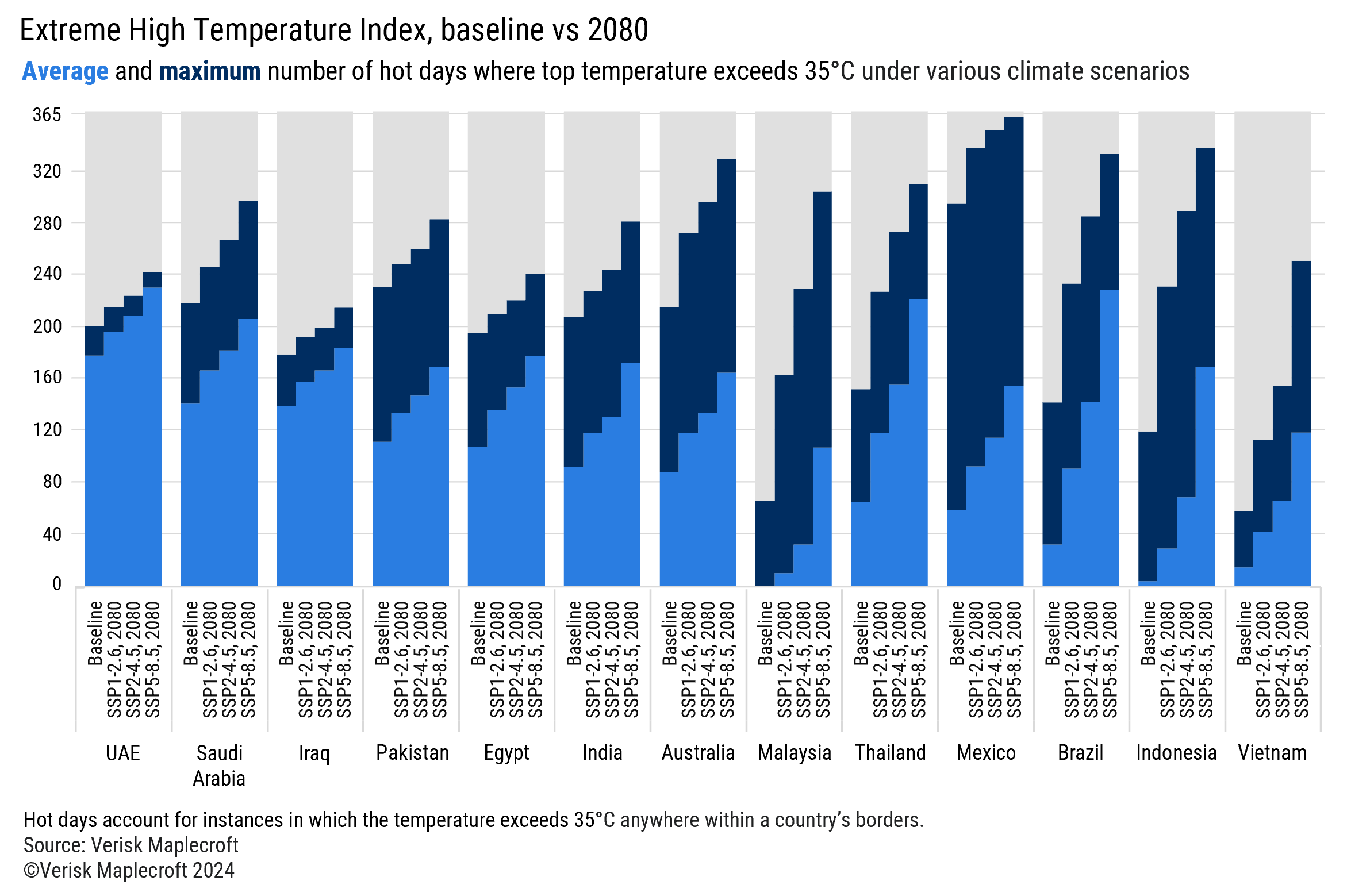

More frequent and intense extreme weather events will be damaging, but heat itself is likely to be the single biggest threat to economic activity, and indeed human life in these countries. Alongside increasing mean temperatures, data from our Extreme High Temperature Index shows that the 13 most climate-exposed major emitters are set to experience a significant rise in episodes of extreme heat. This is shown in Figure 2, which compares the historical baseline against three 2080 physical risk scenarios in relation to both the average and maximum number of days in which temperatures exceed 35˚C.

All are set to see material increases in average hot days per year. But averages do not tell the whole story. Indeed, the potential maximum number of hot days by 2080 (under the worst-case SSP5-8.5) could extend to almost the entirety of a bad year in different regions of countries like Malaysia, Indonesia, Mexico and Brazil.

Extreme heat will act as a pervasive drag on many types of economic activity. This is particularly true when it combines with intense humidity in tropical regions or radiant heat in deserts. These conditions can generate physiological heat stress severe enough to be dangerous for those working in sectors involving outdoor or unventilated work, such as agriculture and construction. Tellingly recent research published by the American Physiological Society suggests safe temperature limits for heat stress may be lower than traditionally thought for young healthy adults – and more so for unhealthy, obese or ageing workforces.

Domestic consequences, global ramifications

The direct and indirect impacts of increased climate hazards in these high-emitting countries are significant. A late or weak energy transition will likely dent productivity anywhere outside air-conditioned offices or factories.

It could drive surges in excess deaths, shut economic activity down for extended periods, and potentially trigger political or migration crises, particularly in middle-income nations with less adaptive capacity. Multinational organisations and investors will also have to factor these exposures into their strategic decision-making or risk long-term threats to resilience.

Split priorities among the ‘drivers’ and ‘sufferers’ of climate change have characterised the COP process to date. But the overlap between the two could, optimistically, reinvigorate stalled global progress. Alternatively – and more realistically – self-interest could become even more entrenched. And, with a host of key elections on the road to COP30, the end of next year could present an even more complicated path towards global carbon reductions.