Emerging market hard currency debt has so far escaped the worst of the fallout from the war in the Gulf. Off the back of announcements by Washington, markets are now pricing in a brief war with contained energy supply impacts which delays rather than reverses Fed easing. But that is far from certain. With no off-ramp for the conflict currently in sight, a major energy and food price shock is a realistic prospect that would force a wider review of EMs’ economic and political resilience by investors.

Our political risk data shows that tail risks extend well beyond the usual suspects. Turkey and multiple other Latin American and emerging European issuers, which tend to move broadly in line with their EMBI benchmark, would be vulnerable to civil unrest that could undermine political and policy stability. If the war stretched out to months, food prices would also become an additional flashpoint for issuers with weaker fundamentals, especially if El Niño compounds supply shortages later in the year.

Barrel half-full

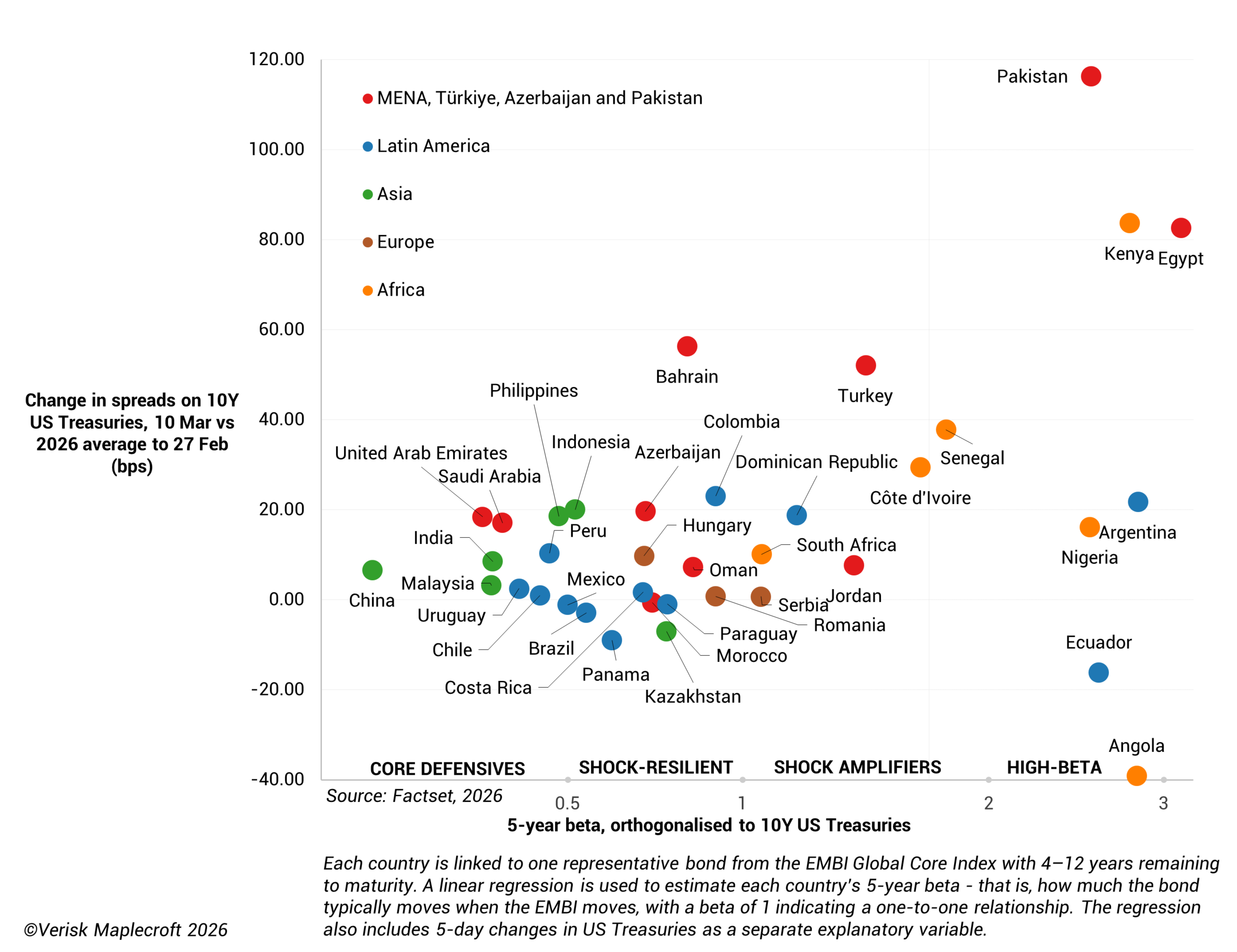

By close on Tuesday 10th March, the yield to maturity of the JP Morgan EMBI Global Core Index stood 17bps higher than on the eve of the US-Israel attacks: a significant change, but far short of last year’s tariff jitters. There has been no risk-off rout: Figure 1 shows that Tehran’s retaliatory missile targeting, countries’ oil trade balance and LNG dependence, and the vulnerability of currencies to a strengthening dollar have driven selective spread widening. Pakistan, already fragile and highly dependent on Gulf energy, has fared the worst.

Civil unrest and food insecurity are the portfolio-wide risks to watch

But what if market optimism is misplaced? Our base case is that the war will last 1-2 months. However, while Washington remains vague on the endgame, Israel wants to remove or permanently weaken the regime. Iran has made clear its existential commitment to the fight and that the war will end on its terms.

If the conflict causes extended disruption to energy trade and infrastructure, financially material impacts on GCC issuers are likely. But that’s only part of the story. The impact on inflation in many emerging markets would be well above 100bps, widespread risk-off spread widening would occur, and emerging market sovereigns would be subjected to a significant stress test.

That is, of course, a big if. But the Goldilocks conditions enjoyed by EM debt investors until end-February are already likely over given the impact of the war so far on market expectations for DM rates pathways. Amid a plethora of looming political and geopolitical risks, now is the time for sovereign investors to assess the broader resilience of their portfolios.

Macroeconomic fundamentals aside, our political risk data indicates that tail risks could manifest in surprising places if any future risk-off shock is inflationary in nature.

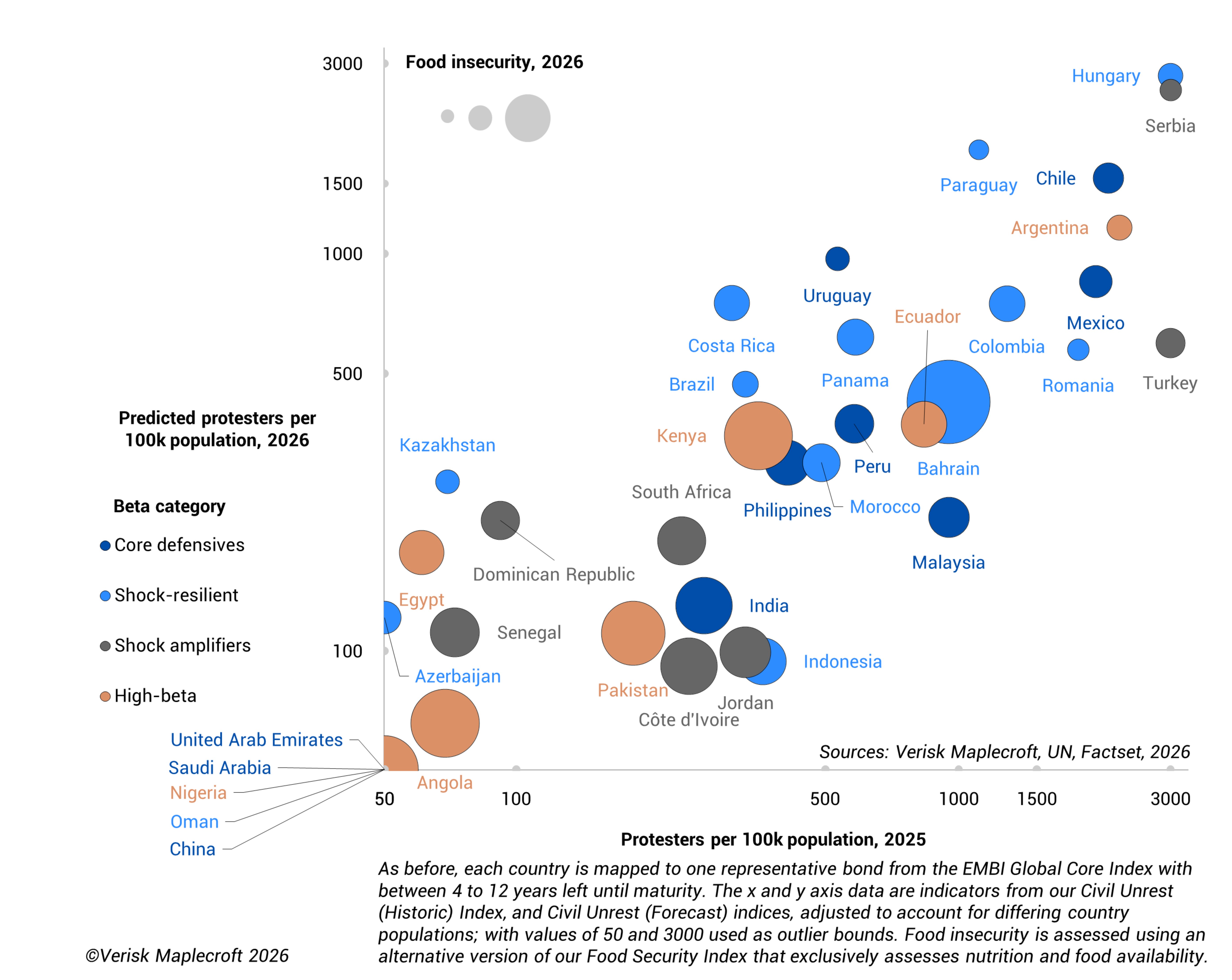

Figure 2 charts the same EMBI issuers according to 2025 levels of civil unrest, forecast 12-month levels as of 2026-Q1, and each’s level of food insecurity. Consumer price inflation is one of the features of our predictive civil unrest model, used to generate the y axis data, and for almost all countries tends to exacerbate unrest.

Almost all the most volatile issuers experience less civil unrest under normal conditions, but have high food insecurity. Food prices are one of the most important components of inflation baskets, and the Iran war looks likely to hit food production by driving global fertiliser shortages. Compounding the longer-term risks, El Niño, estimated by the ECB to increase global food prices by 3% to 9% depending on its strength, has an above-average probability of beginning in H2. If food prices do spike, then we would still expect countries such as Pakistan, Kenya, Côte d’Ivoire, Angola, the already-distressed Senegal and potentially even South Africa to be vulnerable to civil unrest and potential political instability.

As the data shows, it would be a mistake to limit concern to Pakistan and higher-yield African issuers. A range of mostly democratic countries with more stable bond prices, including Turkey, emerging Europe and many Latin American issuers, experienced more unrest than their more volatile counterparts in 2025 and are on track for similar outcomes in 2026. This matters: our 2026 predictions pre-date the conflict, meaning any inflationary impacts of the war on civil unrest would likely be additional. Despite better food security in these countries, any food price rises would still likely exacerbate unrest. Only Ecuador, with its dollarized economy, and politically stable Uruguay would be somewhat shielded.

Finally, Bahrain – with debt already under pressure because of Iranian retaliation – stands out as facing both elevated baseline civil unrest risks and significant food insecurity. The relative deprivation of marginalised Shia communities in this respect adds another dimension of risk.

Positioning for resilience

Preparing for a scenario of the kind outlined above might involve tilting towards some key exporters of energy and soft commodities, as also countries with competent and agile central banks; and reviewing inflation, currency and oil price hedges across the board. But adjusting exposures in line with underlying levels of political resilience, whether via our civil unrest data or one of the many other quantitative political risk metrics we bring to bear on portfolios, needs to be part of the mix as well.