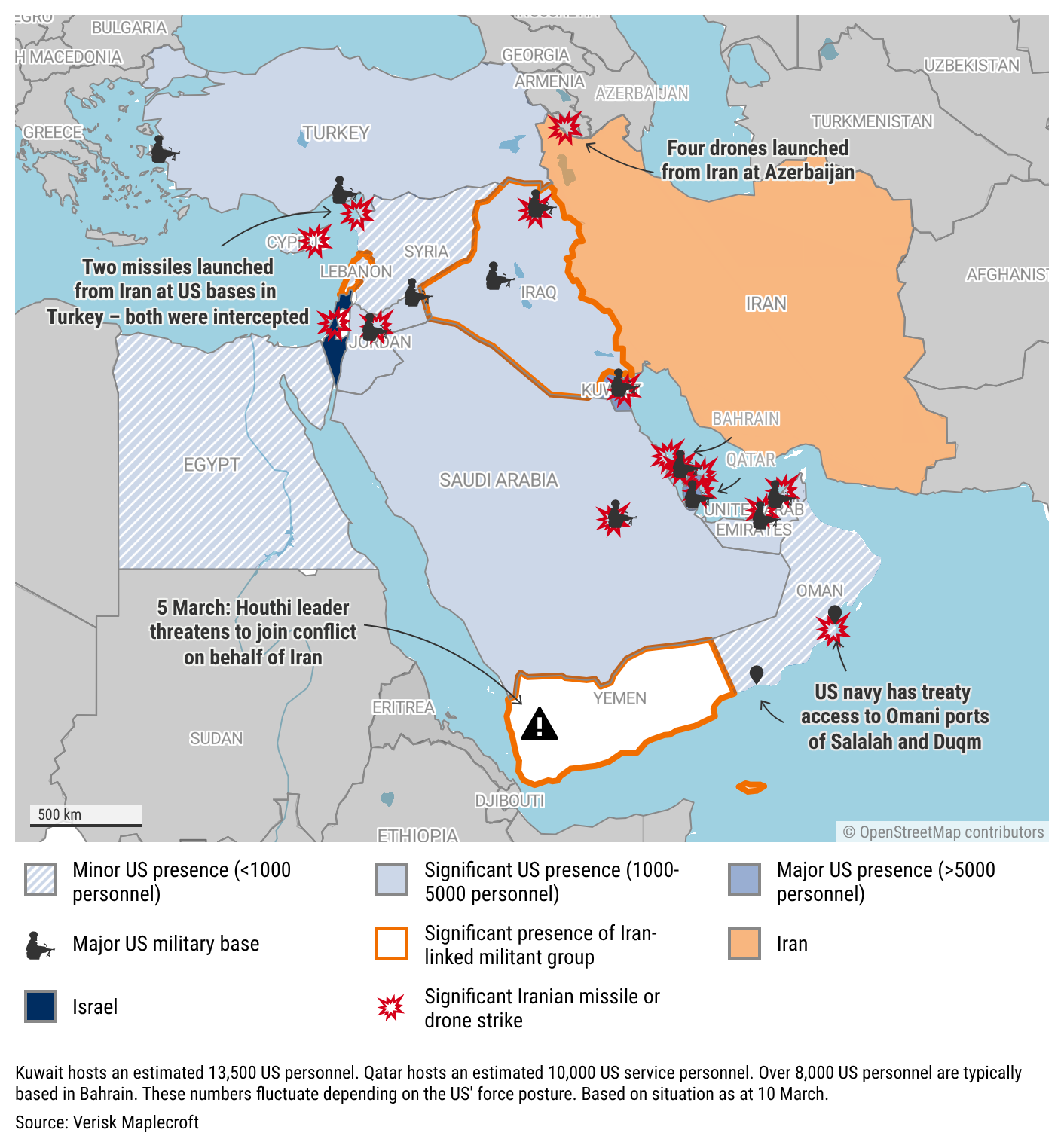

Less than two weeks after the start of US and Israeli strikes against Iran, the economic impact of the conflict is already global in scope. Iran’s rapid and extensive retaliation against shipping and regional energy, port and economic infrastructure has severed a vital artery in global supply chains, as the flow of oil, refined products, LNG and chemicals grinds to a near halt.

The results have been stark: sharp oil price swings, a doubling of benchmark gas prices, downwards pressure on stock markets, and a growing number of declarations of force majeure both in the Persian Gulf and in Asia, as industrial facilities are forced to shut down.

With the global impact of the conflict intensifying day by day, the absence of any immediate off-ramps is a concern for commodity markets, supply chains, and the global economy.

Direction of conflict in next two weeks will be crucial

Gulf officials are warning that the lack of exports will hit revenues, which could compel regional leaders to scale back investments around the world, including in the US. The warning is also likely to be designed to put pressure on the US to find a solution to the ongoing conflict, which has so far imposed a heavy economic cost on the Gulf states.

Conversely, there is also a significant risk that oil and gas prices spike again, especially if routes that are being used to divert exports around the Strait of Hormuz are targeted.

A drone strike against the Ruwais refinery in the UAE – the largest in the region – on 10 March is another reminder that Iran continues to target and damage critical energy infrastructure even if the number of missiles and drones are falling.

Bringing back disrupted supply will take several weeks even in best-case scenario

Oil prices will remain volatile for as long as Iran is able to launch missiles and drones and threaten shipping. Even if the frequency and intensity ease, additional attacks against critical energy infrastructure could trigger further sharp price spikes. Trump’s statement that the war will end “very soon” has brought Brent crude back below USD100 per barrel, but it is still unclear how and when the conflict will be concluded. It is also not a given that Iran will back down even when the US and Israeli bombing stops.

Discussions on the potential coordinated release of emergency reserves have already had an effect, but another push past USD100 is likely if the conflict continues in the same pattern over the coming days. If the situation remains unchanged for several weeks, USD150 per barrel could come into view.

State-backed war risk insurance and naval escorts – as proposed by Trump – could ease some pressure on commodity prices and global supply chains if they can be implemented, but it remains unclear how either would work in practice. For now, most major shipping lines have suspended operations in the area.

If the next two weeks are similar to what we have seen over the last week, the situation will become much more pressing.

The dynamics outlined above highlight just how quickly geopolitical risks can reshape the operating environment. In our on‑demand webinar, our expert explores these emerging pressures in greater detail, assesses probable developments in the weeks ahead, and demonstrates how our Country Risk Data support resilient decision‑making during periods of volatility. Register your details and watch instantly.